International conference on structures and architecture

Af Bæredygtighedsingeniør Hanne Tine Ring Hansen og Professor Emeritus Mary-Ann Knudstrup fra Aalborg Universitet, World Sustainable Built Environment, Maj 05-09, 2017

Hanne Tine Ring HANSENa, Mary-ann KNUDSTRUPb

aSøren Jensen, Denmark, [email protected]

bAalborg University, Denmark, [email protected]

ABSTRACT: The identification of the most effective drivers of sustainable development is a focal point for most – if not all – policymakers and companies interested in sustainable development. Whilst the answer to this is of course very contextual this paper presents a practitioner’s review of the political and voluntary drivers for sustainable building in Denmark.

The paper identifies the most influential drivers for sustainable development in the Danish Building industry by combining a review of the regulatory political drivers in Denmark with two market surveys for construction clients from 2015 and 2016. The result of these surveys is compared to professional experiences from a number of sustainable Danish building projects completed or initiated in between 2008 and 2016.

It is the conclusion of this paper that whilst the regulatory drivers for energy and health are important when it comes to initiating and sustaining the market demand for sustainable buildings it is actually the economic and social drivers for sustainable building, such as life cycle costs, futureproofing of investments, better quality and Corporate Social Responsibility (CSR), that have the greatest impact on construction clients’ decision-making processes. The paper furthermore reflects on how drivers for sustainable development vary depending on the construction client’s planning perspective and how the contractor is engaged in the project.

KEYWORDS: policy and regulation, drivers for sustainable development, strategy development

1. INTRODUCTION

Political and voluntary drivers of sustainable development are essential to whether humankind succeeds in its endeavour to create a more sustainable future in which future generations will not have to pay for the previous and current generations’ over-consumerism and environmental negligence. If these drivers are too ambitious, people give up on delivering the goals set by the policymakers and if the drivers are too conservative the drivers become obsolete or victim of ridicule. By identifying the most effective drivers of sustainable development the chance of finding the right balance between political and voluntary drivers increases.

The following pages will provide readers with an insight into how regulatory and voluntary drivers are perceived by a Danish professional practitioner from the building industry who draws on experiences from more than forty different decision making processes relating to sustainable building design.

2. POLITICAL DRIVERS FOR SUSTAINABLE BUILDING DESIGN

When it comes to political drivers for sustainable development the UN and the EU have a history of providing effective political drivers for sustainable development. The UN has had a great impact on sustainable development through publications like the Brundtland Report and the fourth assessment report from the IPCC panel whilst the EU has made a significant impact on its member states’ energy-efficiency and CO2 reductions in the Building Sector.

From a Danish building practitioner’s point of view, the following EU policies have had the largest impact on sustainable development in the Danish building sector until 2016; the 2010 Energy Performance of Buildings Directive and the 2012 Energy Efficiency Directive. The past two years have also demonstrated how the voluntary UN Global Compact and EU directive on Non-Financial Reporting have established an increased awareness about social, as well as, economic and environmental sustainability with construction clients and tenants. This has increased the market demand for sustainable buildings and changed the scope of sustainable building design from energy-efficiency towards a recognition of more holistic sustainable solutions. Last but not least the EU’s focus on circular economy, the 7th Framework Programme and the Integrated Product Policy have 1) Provided building designers with incentives to design buildings for low-impact and for disassembly and reuse, 2) Caused the Danish government to change its policies on waste management in general and on construction projects and 3) Provided building product manufacturers with incentives to ensure recycling of resources and the use of renewable energy in their manufacturing processes.

3. VOLUNTARY DRIVERS

Since the mid-1980s when the concept of a ‘low-energy building’ was introduced in the Danish Building Regulations Danish building designers and construction clients have had voluntary schemes that have ensured improved the energy-efficiency of the Danish building sector. The scope for sustainability was broadened in 2006 when the Nordic Ecolabel (also known as the Swan Label) was introduced for single family homes in a Danish project titled ‘Future Single-family Homes’. During the period leading up to the release of the Danish version of the DGNB system in 2012 Denmark saw the first BREEAM International and LEED registered projects and the transformation from low-energy towards a more holistic approach to sustainable building design was complete.

Despite having a nationalised adaptation of the DGNB system available and despite the fact that the LEED system is not the most ambitious certification system in a Danish context some companies still choose to adhere to the LEED system when it comes to sustainable building certification or company policies on sustainable building concepts. Based on experiences with companies like these it is this author’s experience that the reasoning behind this choice is strategic and market driven rather than ignorance.

In 2015, the Danish Association of Construction Clients (DACC) conduced a market analysis of how 1) Construction clients, 2) Consultants, 3) Contractors and building product manufacturers perceived sustainability. The survey results are available at DACC’s webpage and the results of the survey show that:

- 65% of construction clients regard the term sustainability as a relevant issue in their project organisations

- 62% of the construction clients define their approach to sustainability as a holistic and integrated approach to sustainability and that 53% of the construction clients define their approach to sustainability to include energy-efficiency

- The construction clients identify life cycle costs (LCC) (61%), total value (51%), branding (54%) and future regulatory requirements (32%) as drivers for sustainable development.

In 2016, the Danish Green Building Council followed up with a market analysis in which:

- 75% percent of the construction clients revealed that they expect the demand for sustainable buildings to increase and 25% expect the demand to remain at its current level.

- The construction clients with experiences with sustainable construction were asked to identify which of the following drivers that motivated them to choose sustainable building certification: environmental considerations (65%) lifecycle costs (48%), CSR (44%), Innovation (41%) Future regulations (37%), Fewer construction and design mistakes and a leaner process (27%), Increased sale and leasing opportunity (24%), increased market value (20%), increased demand for sustainable buildings (20%), 3rd party verification (17%).

The answers to these surveys demonstrate that whilst environmental benefits, as well as, current and future regulatory and voluntary drivers are considered important by construction clients’ they also place great emphasis on economic drivers as well as tenant requirements which typically focus on social- and economic considerations such as operation costs, indoor climate and health. It is also worth noticing that the market analysis from 2015 did not focus on identifying the drivers of sustainable development but rather the main motivation and that the answers were slightly limited by the pre-defined answers in the survey.

4. THE IMPORTANCE OF MARKET, CULTURE AND ORGANISATION

4.1 The importance of market scope

The market scope of the construction client or tenant is essential when it comes to sustainable development where multinational co-operations or multi-nationally funded or insured co-operations in Denmark tend to choose the American LEED system whilst the nationally focused co-operations and organisations adhere to the Danish version of the DGNB system. The general impression of the development in Denmark is that LEED and DGNB are the main players in the market and other systems like the Swan Label, the Passive House and Active House concepts also appeal to some construction clients. This was confirmed in the DACC market analysis from 2015 where the construction clients have answered that 0% favour BREEAM, 14% favour LEED, 71% favour DGNB and 29% favour another system.

Sustainability consultants thus experience different market-driven approaches to voluntary certification schemes: 1) Nationally focused clients that choose to comply with the Danish version of the DGNB system, 2) Multi-national co-operations that choose to adhere to the LEED system because that simplifies their decision making process and thus their building design paradigm 3) Multi-national co-operations that choose to adhere to the scheme that is the preferred, and often most ambitious scheme, in the country where they planning a new project and 4) Multi- national co-operations or national co-operations that wish to comply with more than one scheme e.g. both the Danish DGNB scheme and the American LEED scheme.

Market scope and uniformity are thus important motivators when it comes to voluntary schemes that promote drivers of sustainable development. This also means that the voluntary drivers of sustainability vary a lot from project to project.

4.2 The importance of culture

When looking at the number of buildings in Denmark that have either undergone certification or that are registered for certification there is an increase in the number of tenders and projects that request sustainable building certification. However, if one only regarded the number of projects registered for certification one might think that neither DGNB nor BREEAM or LEED is very popular in Denmark when in fact most construction clients or tenants request sustainability these days. The difference between the Danish market and international markets with a large percentage of certified buildings can be ascribed to the fact that Danes are still a very trusting people. Because of that they regard certification as a stamp of approval of something that they expect their consultants and contractors to comply with regardless of whether or not they request building certification.

This means that voluntary building certification becomes a motivational driver when the construction client or tenant either 1) Wishes to brand his/her property via third party certification or 2) Wishes to change business as usual and challenge his/her organisation, consultants and contractors to improve their performance towards a more sustainable development. The latter is especially true for clients that take CSR reporting seriously and thus have a need to monitor and report progress. It is also interesting that, after having worked for the same companies more than once and having seen multiple tender material from the same clients, a lot of developers and municipal construction clients start out with the first type of motivation and end up with the latter. This is a testament to the fact that once they gain a better understanding of their approach to sustainability they start to use it as a developmental driver.

4.3 The importance of project organisation

Sustainable development is closely related to change management in the sense that sustainable development is about challenging the status quo and ensuring a change towards a more sustainable development. This means that ownership and communication are essential success parameters that one needs to consider when designing a project organisation for sustainable building project. Experiences with both successful and non-successful processes for decision making on sustainable building projects have verified that this is definitely the case when it comes to sustainable development in the building sector.

If the project organisation does not support a shared ownership or the person responsible for realising the sustainability strategy are placed inappropriately in the project organisation the drivers for sustainable development change during the process at the risk of compromising the original intent behind the selected drivers. This means that the project organisation greatly influences the relevance and appropriateness of the drivers of sustainable development and whether the sustainability strategy for a given project is realised.

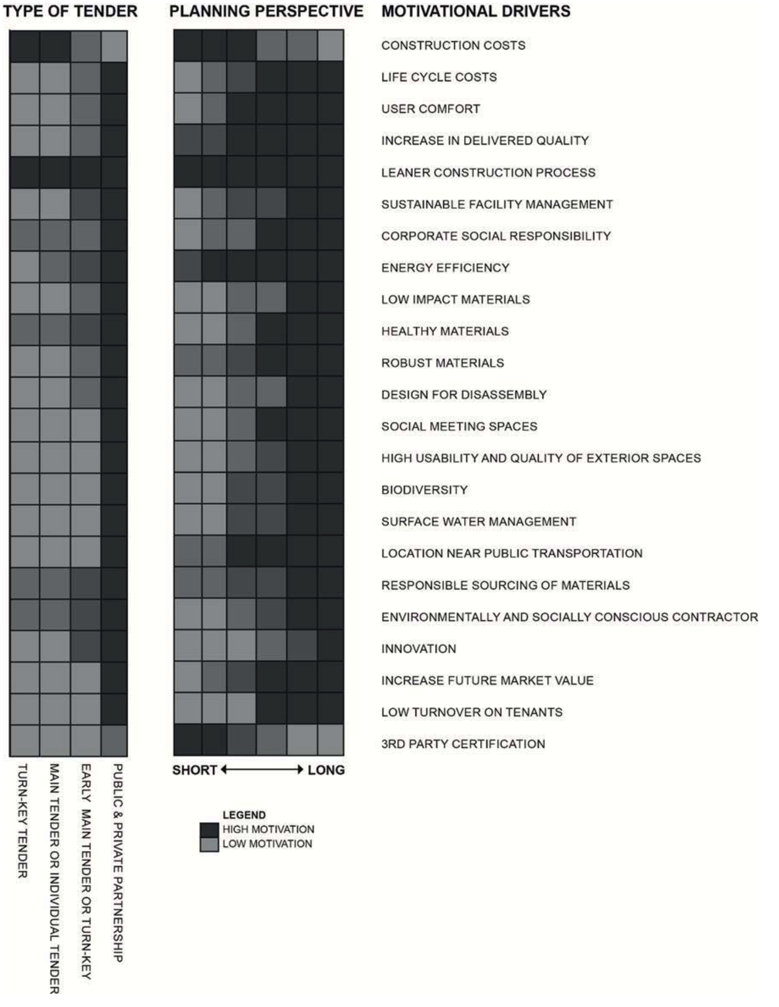

When deciding on a project organisation and a type of tender (i.e. turn-key vs. main-contractor vs. multiple individual contractors) one must therefore consider what motivates the different stakeholders at their given role in the project. Sustainable development is possible no matter the selected type of tender but it is important to be aware of motivational factors and how to ensure ownership with all stakeholders and actors involved in the process when designing the tender material.

Table 1 provides an overview of the experienced drivers for construction clients and an overview of the experienced drivers for contractors depending on the type of tender. The tables are based on experiences with more than forty cases of which at least twenty have either undergone BREEAM, LEED or DGNB certification or used the systems as a strategic tool whilst other projects have included a bespoke evaluation system that builds on one or more of these schemes. The table content for each type of project organisation has been generalised which means that the majority of the evaluated projects correspond with the experiences.

Generally, there are two types of construction clients; 1) Short-term perspective clients and 2) Long-term perspective clients. Short-term perspective construction clients are clients that build with the intent to sell (e.g. developers) whilst long-term perspective clients are clients that build and operate their own buildings (e.g. municipal, regional and social housing organisations).

Contractors are engaged in many different ways and at both early and late stages of the planning process. Generally, the earlier the contractor engagement the better the chance of realising holistic sustainability strategies. Four different types of contractor engagement are used in Denmark; 1) Turn-key contraction, 2) Main contraction, 3) Individual contraction and 4) Public and Private Partnership contraction. Of these four the Public and Private Partnership is the only type of contractor engagement that ensures a strong engagement in drivers for sustainable development in a long-term perspective because the contractor takes on the role of the building owner where he needs to ensure the building operation in a long-term perspective.

Table 1 The experienced correlation between planning perspective and motivational drivers for sustainability and the experienced correlation between type of tender and contractor’s motivational drivers.

5. REFLECTION

This paper compares the practical experiences of a practitioner specialised in sustainable building design with political and voluntary drivers in the Danish building sector.

When creating strategies for sustainable building projects Construction clients and client consultants need to be very careful when designing their project organisation and tender material. Drivers for sustainable development must be identified and prioritised in the initial ideation stage of all projects and an implementation strategy must be developed for the selected project organisation and the type of tender. Contractor motivation must be considered in this process to ensure that the Construction Client’s drivers for sustainability also motivates the contractor (e.g. by early engagement of the contractor or financial incentives to perform better).

When it comes to the political drivers for sustainable development a lot of clients are not conscious of EU or UN enforced drivers. They do however still have an impact on the construction client’s decision making because they are influential of the Danish building regulations which the market analyses from 2015 and 2016 have verified that construction clients are very much aware of.

When reflecting on which drivers are the effective it is positive to see that the political drivers and the voluntary drivers together ensure a market demand that in turn engage construction clients and tenants to implement voluntary schemes in their projects. In the past decade, the market reached a tipping point where voluntary economic and social drivers of sustainable development became strong and well-known drivers for sustainable building. Energy efficiency of buildings is still a strong driver but that has more or less become a standard requirement in all building projects which motivates construction clients to differentiate themselves more on the social and economic drivers.

Education of construction clients is also relevant due to the importance of early identification and implementation planning of motivational drivers. Today the client consultant, the architect or engineer takes on the role of educator which means that the construction client’s knowledge is limited to the expertise of the consultants engaged on the project.

REFERENCES

[1] Active House, Active House [Online] Retrieved from: http://www.activehouse.info/ [Retrieved on September 30, 2016]

[2] BRE, BREEAM [Online] Retrieved from http://www.breeam.com/ [Retrieved on September 28, 2016]

[3] Bygningsreglementet.dk, Bygningsreglementet 1985 [online] Retrieved from

http://w2l.dk/file/502104/br_femogfirs.pdf [Retrieved on September 28, 2016]

[4] Danish Association for Construction Clients, Hvidbog [Online] Retrieved from

http://www.bygherreforeningen.dk/projekter/baeredygtighed-i-byggeriet [Retrieved on September 28, 2016

[5] Danish Green Building Council, an introduction to DGNB [Online] Retrieved from: http://dk-

gbc.dk/publikationer/an-introduction-to-dgnb/ [Retrieved on September 27, 2016]

[6] Danish Green Building Council, Markedsundersøgelse 2016 [Online] Retrieved from http://www.dk-

gbc.dk/media/2100/markedsundersoegelse_web.pdf [Retrieved on September 28, 2016]

[7] Ecolabel.dk, Bygninger [online] Retrieved from http://www.ecolabel.dk/da/produkter/byg-og-bolig/bygninger [Retrieved on September 28, 2016]

[8] European Commission, 7th Framework Programme [Online] Retrieved from

https://ec.europa.eu/research/fp7/index_en.cfm [Retrieved on September 28, 2016]

[9] European Commission, Energy Efficiency Directive [Online] Retrieved from: http://eur-lex.europa.eu/legal-

content/EN/TXT/?qid=1399375464230&uri=CELEX:32012L0027 [Retrieved on September 28, 2016]

[10] European Commission, Energy Efficient, Buildings [Online] Retrieved from:

https://ec.europa.eu/energy/en/topics/energy-efficiency/buildings [Retrieved on September 28, 2016]

[11] European Commission, Energy Performance of Buildings Directive [Online] Retrieved from: http://eur-

lex.europa.eu/eli/dir/2010/31/oj [Retrieved on September 28, 2016]

[12]European Commission, Environment [Online] Retrieved from:

http://ec.europa.eu/environment/index_en.htm [Retrieved on September 28, 2016]

[13] European Commission, Integrated Product Policy [Online] Retrieved from

http://ec.europa.eu/environment/ipp/epds.htm [Retrieved on September 28, 2016]

[14] European Commission, Non-financial Reporting [online] Retrieved from: http://ec.europa.eu/finance/company-reporting/non-financial_reporting/index_en.htm [Retrieved on September 28, 2016]

[15] European Commission, Towards Circular Economy [online] Retrieved from: https://ec.europa.eu/priorities/jobs-growth-and-investment/towards-circular-economy_en [Retrieved on September 28, 2016]

[16] Intergovernmental Panel on Climate Change, Fourth Assessment Report [Online] Retrieved from http://www.ipcc.ch/report/ar4/ [Retrieved on September 28, 2016]

[17] Kotter, J. P 2012, Leading Change, USA.

[18] Passiv Haus Institute, Home [Online], Retrieved from: http://www.passiv.de/ [Retrieved on September 30,

2016]

[19] United Nations, Our Common Future [Online] Retrieved from: http://www.un-documents.net/our-common-future.pdf [Retrieved on September 28, 2016]

[20] United Nations, UN Global Compact [Online] Retrieved from: https://www.unglobalcompact.org/ [Retrievedon September 28, 2016]

[21] US Green Building Council, LEED [Online] Retrieved from http://www.usgbc.org/leed [Retrieved on

September 28, 2016]

[22] US Green Building Council, LEED project directive [online] Retrieved from http://www.usgbc.org/projects

[Retrieved on September 28, 2016]